UiPath’s revival strategy, led by CEO Daniel Dines, focuses on AI integration and partnerships like SAP to overcome challenges and drive growth. See more here.

By Fountainhead

I first bought and recommended UiPath (NYSE:PATH) around September 2023, at $17.75 per share. The stock peaked at around $27 in Feb 2024, and then drifted downwards; The advent of Generative AI becoming a possible threat to Robotic Process Automation created doubts about whether UiPath could sustain its momentum in a fiercely competitive field where it was the leader.

These were the reasons why I liked the RPA leader, then

While I did feel that low-hanging fruit in automation or workflow processing could be captured by Generative AI, and over time get commoditized, I felt strongly that UiPath could infuse AI to make its products so much better, customized and a differentiator offering more savings. It had the potential to do so because of its large client base, access to its data, workflows, and solutions, and a history of automating its processes. That I feel is the real competitive advantage it has over generative AI.

I believe UiPath has AI leadership for business use cases and augmenting their processes with AI will be a strong tailwind and foundation for business solutions for the next decade.

Generic AI cannot solve the complexities within organizations but a seasoned RPA player like UiPath can customize and improve their existing solutions for clients looking for AI solutions to save costs. A player like UiPath, that can further simplify or automate business processes or tasks will make it the differentiating factor and a moat, which others won’t have.”

They generally offer end-to-end automation capabilities, as a one-stop shop, which is a competitive advantage because switching costs are high, and other vendors and competitors tend to specialize in a few areas. Some of their competitors offer extensions of their core competencies, for example, IBM has low code IBPms, and Celonis Inc, has process mining, but UiPath offers more use cases within organizations as their core strength. There is a seamless and versatile integration, which is often a selling point with customers.

But, around Q2-2024, UiPath took a U-turn, burnishing a stellar, sturdy start-up story with a massive revenue miss and guidance, which the wider analyst community, including me, never saw coming (some analysts, huh!). The stock tanked from $20 to $12 in a matter of days and saw founder Daniel Dines returning as CEO to right the Titanic from keeling over.

What caused UiPath to miss revenue estimates so badly?

A combination of reasons:

Sales Execution: Under CEO Rob Inslen, who helmed the company for two years, growth hadn’t deteriorated, and quarterly sales growth for the past 4 quarters had grown between 18% and 31% – even as it became lumpy, which happens with enterprise SaaS businesses. The April 2024 quarter did show weakness at only 16% growth, but it was the guidance of 10% growth for the July 2024 quarter and full-year guidance for FY2025 at just 10-11% that showed that indeed UiPath’s sales team was having a hard time with:

- Increased scrutiny of deals, indicating a more cautious approach from potential customers.

- Lengthening sales cycles for large multi-year deals, suggesting hesitation from clients.

- Reduced deal sizes: Several large expansion deals closed with smaller sizes than anticipated.

Competition: UiPath competes with the 800-pound gorilla Microsoft (MSFT), Automation Anywhere, Blue Prism, and Appian (APPN). My survey and analysis of users on Reddit suggest that while UiPath is an excellent and often preferred solution, it’s expensive and geared toward larger companies that can absorb higher licensing costs. Often, competitor Microsoft is preferred because it is also more closely aligned with other Microsoft products such as Azure and 365. The other advantage Microsoft has is that it can bundle RPA with other products and absorb longer sales cycles, without affecting its quarterly bottom line – a luxury UiPath cannot afford.

Generative AI: While management strongly defended Its products as AI-infused and also cited NRR of 113% to 115% and ARR growth between 14% and19% as support that Generative AI was not chipping away at their customer base, there remain lingering doubts that UiPath could be ceding ground to low-hanging fruit, which didn’t need an expensive license, and whether UiPath was generating enough efficiencies or savings for clients. If nothing, increased scrutiny and lengthening sales cycles did suggest that customers were looking at Generative AI tools as a cheaper alternative to help them automate some manual business processes, identify repetitive tasks, write automation rules, and implement software-driven solutions.

October quarter, Q3-FY2025 – Getting back on its feet.

As of Jan 15th, 2025, the stock has recovered from its 2024 August, low of $10.37 to $13.50, and Q3-2025 earnings and revenues have beaten estimates as below:

- Revenue of $354.65Mn (+9% YoY) beat by $6.93M.

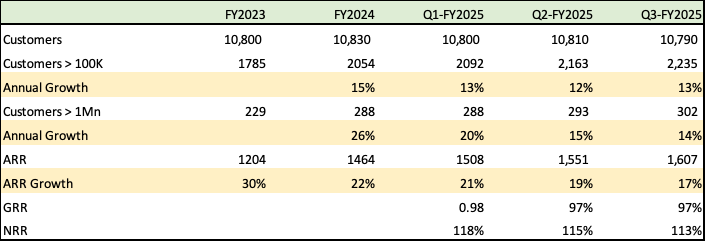

- ARR of $1.607 billion (+17% YoY) is in line with the previous estimate of #1.603Bn. ARR growth at 17% continues to be much stronger than revenue growth of 9%, which is common in SaaS, companies who have to follow 606 revenue accounting standards.

- Net new ARR of $56 million.

- Dollar-based NRR of 113%; while this is lower than Q2’s 115%, management indicated confidence that it would stabilize in FY2026 to previous levels.

- Non-GAAP gross margin was 85 percent. Slightly better than the 83-84% average in the past few years.

- Non-GAAP operating income was $50 million.

- Net cash flow from operations was $28 million – In FY2024, UiPath generated $300Bn in cash flow and expects to generate $350Bn in FY2025

Guidance for Q4-FY2025 and FY 2025:

- Revenue – $422Mn to $427Mn V consensus of $424.03M. In line with estimates.

- ARR $1.669Bn to $ 1.674Bn as of January 31, 2025, at a mid-point of 1.715, it is slightly higher than the previous guidance of $1.668Bn.

Strategic changes bode well for the company

UiPath restructured its leadership last summer, with Founder Daniel Dines returning as sole CEO in June 2024 and taking product and sales responsibilities. CFO Ashim Gupta was also appointed as COO, taking dual charge of operations and finance.

These are the ongoing operational improvements and goals:

10% workforce reduction in July – the primary benefit here will be di-siloing and having a clearer road map on sales and marketing. With CEO Dines taking on product and sales responsibilities, a streamlined and focused workforce should interact better with customers, which should translate into improved offerings and competitive advantages.

A focus on profitability – It is targeting a full-year pro forma operating margin of ~12%

Doubling down on reseller partnerships, – In my opinion, the partnership with SAP SE (SAP) is crucial for both SAP and UiPath. SAP has been a legacy enterprise software player for the longest time and one of the leaders in its field, with a gigantic reach into the largest companies.

Is the path ahead smooth or rocky?

Can Dines engineer another U-Turn, this time in the right direction?

Smooth Path

Industry agnostic: One of UiPath’s biggest strengths is that it is industry, client, and workflow agnostic. Its product is fairly user-friendly and clearly identifies solutions regardless of verticals. It aims to become the Switzerland of Agentic RPA and, more importantly, also grow through collaborating with its clients. It doesn’t flinch from working with their client’s legacy systems or collaborating with other vendors dealing with their clients.

Switching Costs: At the end of Q3-FY 2025, they had 2,235 clients with over $100,000 in ARR and 302 clients with over $1Mn in ARR, accounting for 86% of total revenues. These are not easy switches or cheap switches. Further, over 100% NRR indicates that UiPath is landing and expanding and not losing clients.

Jumping on the agentic bandwagon: UiPath has integrated AI Agentic capabilities into workflow automation and combines them with its autopilot functions. Management cited several wins in its Q3-FY2025 earnings call and also indicated that it is moving at an extremely fast pace with over 1,000 sign-ups. A large Fortune 50 healthcare and insurance company signed up to include its Agent build for automation. How does agentic automation help UiPath, and what is differentiated about them? I believe the key differentiators are a) the existing processes that UiPath has already embedded in clients’ workflows, b) A wider array of tools like autopilot and c) A collaborative effort working in tandem including coloration with SAP workflows.

Riding on the SAP train: In Q3-2025, UiPath integrated its platform into the SAP Build Process Automation solution and offers it as an extension with SAP solutions. Given SAP’s massive size of $35Bn in revenues and a market cap of $300Bn — this is a huge opportunity. The value of a seamless experience for several workflows across the organization on a single platform is high for the client, driving efficiency and productivity.

Stable operating metrics and growth in key cohorts

Importantly customers over $100K and $1Mn have grown faster and 13% and 14% respectively, even as the total number of customers have remained stagnant. Also, ARR growth, which is the far more important metric has been 17% far higher than the revenue growth of 9%.

The industry leader

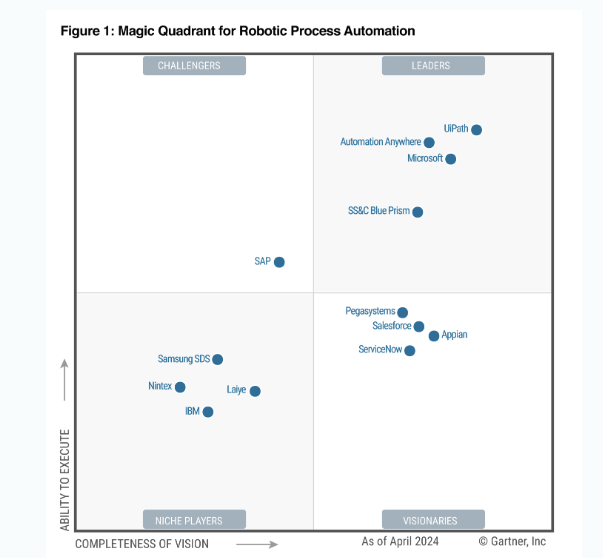

UiPath’s leadership in RPA in Gartner’s magic quadrant in 2024, plays well to, and endorses its expensive, high-quality positioning catering to deep-pocketed client base.

Rocky path

It’s still a show-me story and a 9% revenue growth in Q3-FY2025 means we have a long way to go. We shouldn’t be stuck in a value trap here.

I also found it a bit telling that the Q3-FY2025 presentation focused on Agentic growth, whereas the Q2-FY2025 presentation, has just a few mentions of the word agent. The same goes for the Q-2 transcript.

Is it just rebranding of infused/embedded AI, copilots, and chatbots, or is it real?

You can’t invent a product in one quarter, so I’m skeptical, and I would like to see more details on agentic revenues. Management did talk about reporting separate metrics for agentic revenues, which is a good sign.

Enterprise software is an extremely difficult business and as we saw from UiPath’s metrics, getting large clients to spend an average of $600,000 a year is an extremely difficult job when you’re struggling to show real cost savings or differentiate your product.

Buy UiPath

There are several arrows in their quiver.

I like their agnostic and collaborative approach, really, the Switzerland of Agent collaborations or orchestrating agents across workflow domains and providers.

The partnership with SAP – Any impetus that Salesforce gets will be shared by UiPath. It’s an integral part of the SAP solution and it increases UiPath’s reach tremendously and dovetails perfectly with their strategy to focus on serving the large cohort of clients between $100,000 and $1Mn in ARR, as CFO Ashim Gupta emphasized in a recent conference with Needham. UiPath has been the high-quality, top of its class provider as we saw in the Gartner quadrant and this strategy should reap good dividends for it.

I was also impressed by guidance that net retention rates would start growing in FY 2026

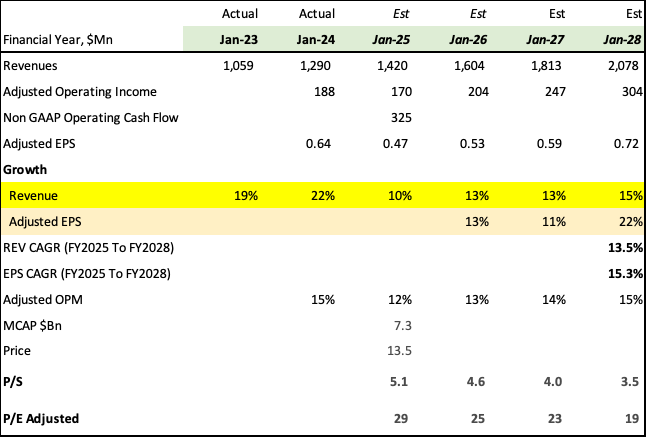

UiPath’s updated financial forecast and current valuation do make a great case for investment as a GARP, now that it’s likely to grow only in the mid-teens, valued at just 5X sales, and 25x adjusted earnings. Besides, cash flow is almost double adjusted operating income, so that too is a plus.

It is a cash-rich company with $1.74Bn in cash, with a mandate to buy back shares, setting a floor for the stock price.

It has a decent margin of safety: It’s just the second quarter from the bottom, and while it does remain a show me story – at this valuation, I am not a seller. I can easily wait a couple of quarters more because I believe there is a limited downside. The market cap of $7.3Bn is just 4.5x its cash.

With strategic actions like the return of the founder to actively managing the company, expenses getting cut, and a commitment towards profitability. It would be meaningless to sell now.

The COO clearly mentioned that there is absolutely no degradation in orders in the earnings call, and they’ve beaten estimates and guidance twice already, just by not very much, and the markets haven’t rewarded them, which is good for a bargain hunter like me, who’s in it for the long haul. I’m own some and continue to buy on declines.